The Australian Tax Office (ATO) states that rental related income "is the full amount of rent and associated payments that you receive, or become entitled to, when you rent out your property, whether it is paid to you or your agent."

Most property investors are pretty clear on what is meant by rent. However, at times the term 'associated payments' confuses investors. Often these payments are withheld from a property investor's tax return which can become a significant issue in the event of an ATO audit.

Associated payments include:

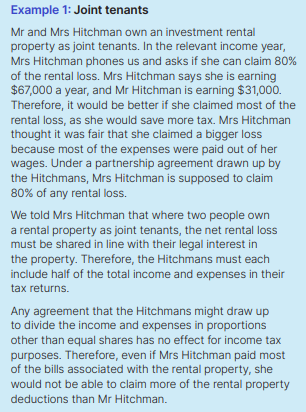

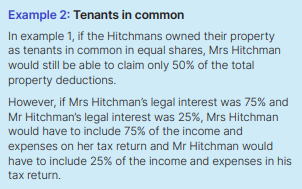

It is important that rental income (and expenses) for tax purposes are divided according to legal interest in the property. There are a number of ownership structures you can elect to buy property in. I refer to these in my book BreakFree Like The 1%.

For simplicity, the following options exist for property investors that choose to own a property in their individual names and are not carrying on a business of letting rental properties:

If you already own property and are not sure what your legal interest is, check the title deed.

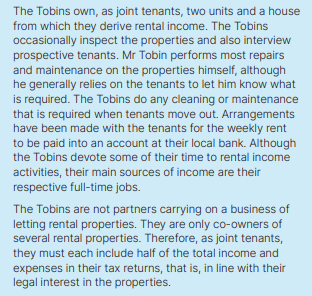

Additionally, property investors are uncertain as to whether they are in the business of letting rental properties, particularly as their property portfolio grows in size and number. The ATO provides guidance on this, as the examples below demonstrate.

The examples above are key considerations when deciding to purchase properties in one's individual name.

As stated earlier, there are a number of different ownership options (including companies and trusts) that an experienced and competent tax accountant can assist you with. Each option has its own benefits and limitations, therefore it is a decision that should be made on an informed individual basis, under the guidance of a licenced professional.

The ATO's publication Rental Properties 2022 is an excellent publication that every property investor should access and read. You can find it here.