The Australian property market continues to be the principal asset class of choice for Australians with 57.0% of household wealth held in housing at a total estimated value of $9.3 Trillion. This is greater than the combined value of Australian Superannuation, Australian Listed Stocks and Commercial Real Estate.

Furthermore, with outstanding mortgage debt currently at $2.1 Trillion, the Australian Residential Real Estate Market has a Loan to Value Ratio (LVR) of 22.6%. Contrary to many mainstream media headlines, the overall market's LVR is not what would be considered to be at critically dangerous levels.

According to CoreLogic, median dwelling values for the Australian property market in the 8 capital cities as of 31 January 2023 were as follows:

| Sydney | Melbourne | Brisbane | Adelaide | Perth | Hobart | Darwin | Canberra |

| $999 278 | $746 468 | $698 204 | $646 045 | $559 971 | $666 431 | $500 228 | $841 605 |

Whilst Sydney continues to have the highest median dwelling value, it is worth noting that despite having the 4th largest population of all the capital cities, Perth's median dwelling value ranks 7th overall. This is approximately 56% of the value of Sydney's median dwelling value, and a staggering $106 460 less than Hobart's median dwelling value which has approximately 10 times less the population of Perth.

Combined regionals (0.8% decrease) outperformed combined capitals (1.1% decrease) during January 2023. The Regional South Australian (0.5%) and Regional Western Australian (0.4%) markets led the way. In the capital city market, no markets experienced growth, whilst Hobart (-1.7%) and Brisbane (-1.4%) suffered the largest decreases in dwelling values.

Combined regionals (2.6% decrease) outperformed combined capitals (3.3% decrease) during the past 3 months to February 2023. The Regional South Australian (2.3%) and Regional Western Australian (1.9%) property markets were the top performers. In the capital city market, Perth (-0.1%) outperformed its peers, whilst Hobart (-5.5%), and Brisbane (-4.8%) both experienced a reduction in dwelling values over the quarter.

Combined regionals (2.3% decrease) outperformed capital cities (8.7% decrease) during the past 12 months to February 2023. The Regional South Australian (15.3%) and Regional Western Australian (4.9%) property markets recorded the highest levels of growth. In the capital city market, Adelaide (6.9%) and Darwin (3.7%) were the standouts, whilst Sydney (-13.8%) and Hobart (-9.5%) experienced the largest decreases in dwelling values over the past year.

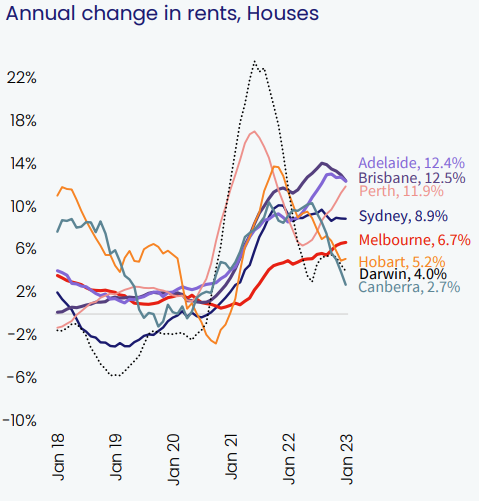

The Adelaide housing rental market continues to charge ahead with a 12.4% growth in rents over the past year. Brisbane (12.5%) and Perth (11.9%) have also experienced substantial growth in rents for houses over the preceding 12 months.

The Canberra housing rental market has been more subdued, growing at 2.7% over the previous 12 months. Darwin (4.0%) and Hobart (5.2%), although at the lower end of rental growth, are also seeing healthy increases in rents for houses.

The Sydney unit rental market has outperformed all other capital cities, experiencing a 15.9% growth in rents over the past year. Continued pressure will be placed on this market as international borders progressively open globally and immigration returns to pre-pandemic levels. Brisbane (15.3%) and Melbourne (13.6%) have also seen substantial growth in rents for units over the preceding 12 months.

Similarly to housing rents, Canberra and Darwin have experienced more moderate growth of 4.7% and 6.0% respectively in unit rents over the previous 12 months. Hobart (8.1%) has continued its annual increase, roughly in line with the economy's broader level of inflation.

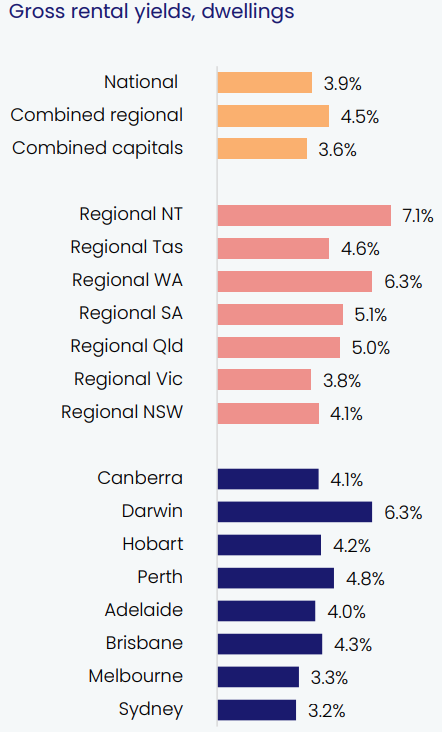

Combined regional yields (4.5%) continue to be higher than combined capital gross yields (3.6%).

Regional Northern Territory (7.1%) and Regional Western Australia (6.3%) collectively have the highest regional gross yields, whilst Regional Victoria (3.8%) and Regional New South Wales (4.1%) have the lowest yields.

Amongst the capital cities, Darwin (6.3%) and Perth (4.8%) continue to offer the best opportunities for investors to purchase positive to neutrally geared property. On the opposite end of the spectrum, Sydney (3.2%) and Melbourne (3.3%) continue to offer the lowest gross rental yields.

Find the full version of the National Media Release by CoreLogic here.

You can find the Property Market Update for December 2022 here.